Anne Smith1 of Rockingham County, New Hampshire, is ready to retire.

After years working in the local court system and with her children grown and away at college or starting their careers, she’s looking forward to more leisure time. But transitioning to a fixed income is also a major concern. Her husband’s health is failing, and Anne is coming to terms with a future alone. She knows her retirement income won’t be enough to pay their existing mortgage each month.

Over the years, she and her husband refinanced twice to pay for his mounting medical bills, leaving little equity for her to downsize or to make the home repairs they have been putting off for years.

What options does she have? Could she qualify for a smaller loan? And if she rented, could she afford the increasing rents in her neighborhood on her retirement income?

Anne, as it turns out, is not alone. Many older adults are facing similar challenges and limited options. Recent research by the Federal Reserve Bank of Philadelphia shows that older adults are more likely to be rejected for most types of mortgages, a trend that becomes increasingly more likely as a person ages. In turn, a lack of access to credit can impact how older adults can afford to maintain and upgrade their homes, tap into equity to pay off medical debts, or find ways to downsize after losing a partner or spouse.

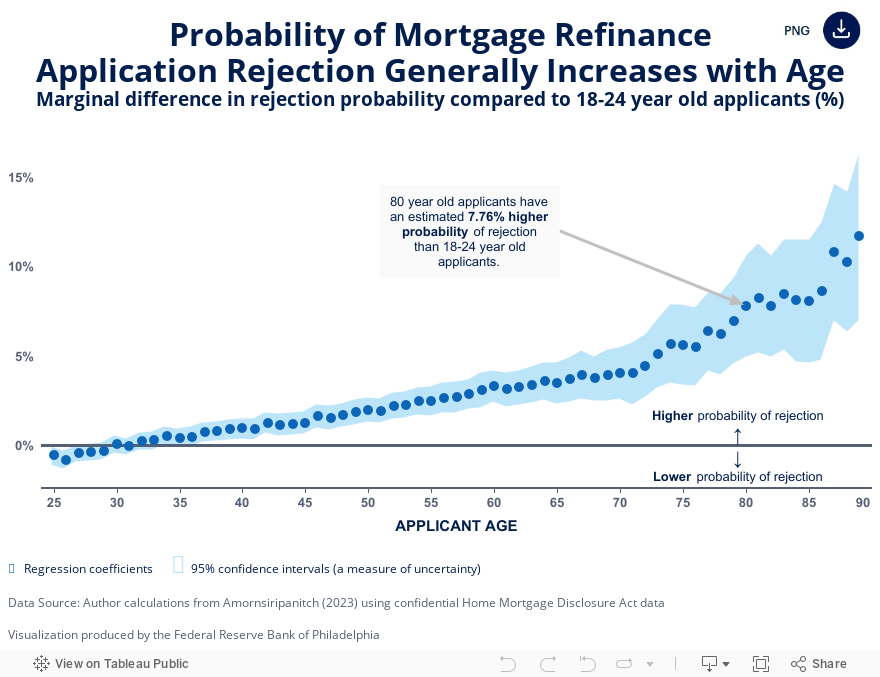

millions of refinance applications

and found rejection rates increased

with age.

For the Philadelphia Fed, understanding these barriers to credit and how they impact people’s lives is a key part of our work to support a strong economy. In a February 2023 working paper, Philadelphia Fed Economist Natee Amornsiripanitch details the age gap in mortgage access. By studying millions of single-borrower mortgage refinance applications gathered through the Home Mortgage Disclosure Act (HMDA), Amornsiripanitch found that mortgage rejection rates increased — and even accelerated — as applicants aged. It was a pattern he found to be consistent for most lenders and many loan types, including conforming, non-conforming, Federal Housing Authority, and Veterans Affairs loans.

“Overall, the results suggest that older individuals systematically face higher barriers to mortgage access,” Amornsiripanitch notes in his paper. In the study, he controls for a wide range of factors including applicant credit scores, property types, and economic and demographic data, allowing him to focus on age and mortgage outcomes.

Yet, Amornsiripanitch points out that the HMDA data are only one piece of a very complex application process and should not be interpreted as definitive evidence of lenders making age-based decisions. Instead, he sees the importance of asking questions about aging and access to mortgage credit, especially as the U.S. housing supply becomes more limited and expensive.

“There isn’t much in the literature that examines the relationship between age and access to credit, mainly because of data constraints,” according to Amornsiripanitch. “But the mortgage market is one of the largest retail credit markets in the nation, and it’s critical that we understand how consumers are experiencing this market and what trends are appearing in the data.”

Home Buyers Are Older

One important trend is the increasing median age of a home buyer. According to the National Association of Realtors (NAR), the ages of a typical first-time and repeat home buyer reached an all-time high in 2022. In 2022, the median age of a first-time home buyer was 36 years old, compared with 29 in 1981, the year the NAR began surveying home buyers. Among buyers who had previously purchased a home, the median age was 59 years old in 2022, a 28-year increase from age 31 in 1981.

While these trends are likely a combination of many social, economic, and environmental factors, it’s important to consider that a typical mortgage term is 30 years. If a buyer purchases a home in their mid-30s and stays the duration, then the homeowner would then likely see their mortgage mature just shy of retirement age — a time when many consider making home repairs or upgrades, consolidating debt to reduce their monthly expenses, or helping family members go to college or buy their own home. All these scenarios may require access to credit, including options to refinance.

In his analysis, Amornsiripanitch points out that older applicants do tend to apply for shorter terms, noting that approximately only 20 percent of loan applications with maturities of 30 years or longer were made by those in the 59 years or older age group.

Loans Are More Expensive

Amornsiripanitch’s analysis also revealed that accessing credit becomes more expensive as people age. In the paper, he points to a 10-basis point difference between the 30-to-39-year-old age group and the 70-plus age group. It’s a significant difference that he acknowledges could be even larger, given that older adults are more apt to purchase, or “buy down,” points than younger home buyers, a trend he noticed in the data.

“One plausible explanation for the higher cost could be less lender research or ‘shopping around’,” Amornsiripanitch writes. “Searching can be costly both mentally and physically, and coupled with less experience with or exposure to technology, older borrowers may perform a less comprehensive search of potential lenders and end up receiving less favorable rates because they cannot provide competing rates for lenders to match.”

The data also suggest higher rejection rates may mean that older homeowners are less able to take advantage of accommodative monetary policy or lower interest rates, which could potentially make retiring on a fixed income more affordable for more people.

Solving for Risk

For Amornsiripanitch, this research highlights a conundrum that many older Americans are increasingly facing. Lenders may see older borrowers as riskier because they may have limited income, higher debt-to-income ratios, less time to repay the loan, and/or in many cases, “insufficient collateral,” a term for an asset that has depreciated below its original loan value, sometimes because of lacking maintenance. This last reason for denial was cited in roughly 50 percent to 70 percent of loan rejections, depending on age group.

“Keeping up with maintenance can often be challenging for older homeowners, particularly if the decision is between fixing the leaking roof or affording one’s monthly medications,” Amornsiripanitch says.

In fact, other research by the Philadelphia Fed estimated the cost of addressing “physical housing deficiencies” nationwide to be upward of $149 billion, an 18 percent increase from the 2018 estimate, according to the March 2023 report.

The U.S. population is aging as the sizable baby boomer generation — and Generation X right behind it — reaches retirement age. Projections show there will be about 80.8 million older Americans by 2040, more than twice as many as in 2000.2 Clearly, there is a need for more discussion and research.

“Given its economic importance and many unexplored potential explanations, the relationship between age and credit access should be an active area of economic research,” Amornsiripanitch concludes, “especially as aging becomes a more pressing policy concern.”

- The views expressed here are solely those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Philadelphia or the Federal Reserve System.

- Anne Smith’s name has been changed to protect her privacy.

- See https://acl.gov/sites/default/files/aging%20and%20Disability%20In%20America/2020Profileolderamericans.final_.pdf.