October 2024 Manufacturing Business Outlook Survey

Note: Survey responses were collected from October 7 to October 14.

Manufacturing activity in the region expanded overall, according to the firms responding to the October Manufacturing Business Outlook Survey. The survey’s indicators for current general activity, new orders, and shipments all rose, with the latter two returning to positive territory this month. The employment index declined and suggested mostly steady employment conditions. Both price indexes edged down but continue to indicate overall increases in prices. Expectations for growth over the next six months were more widespread this month as most future indicators rose.

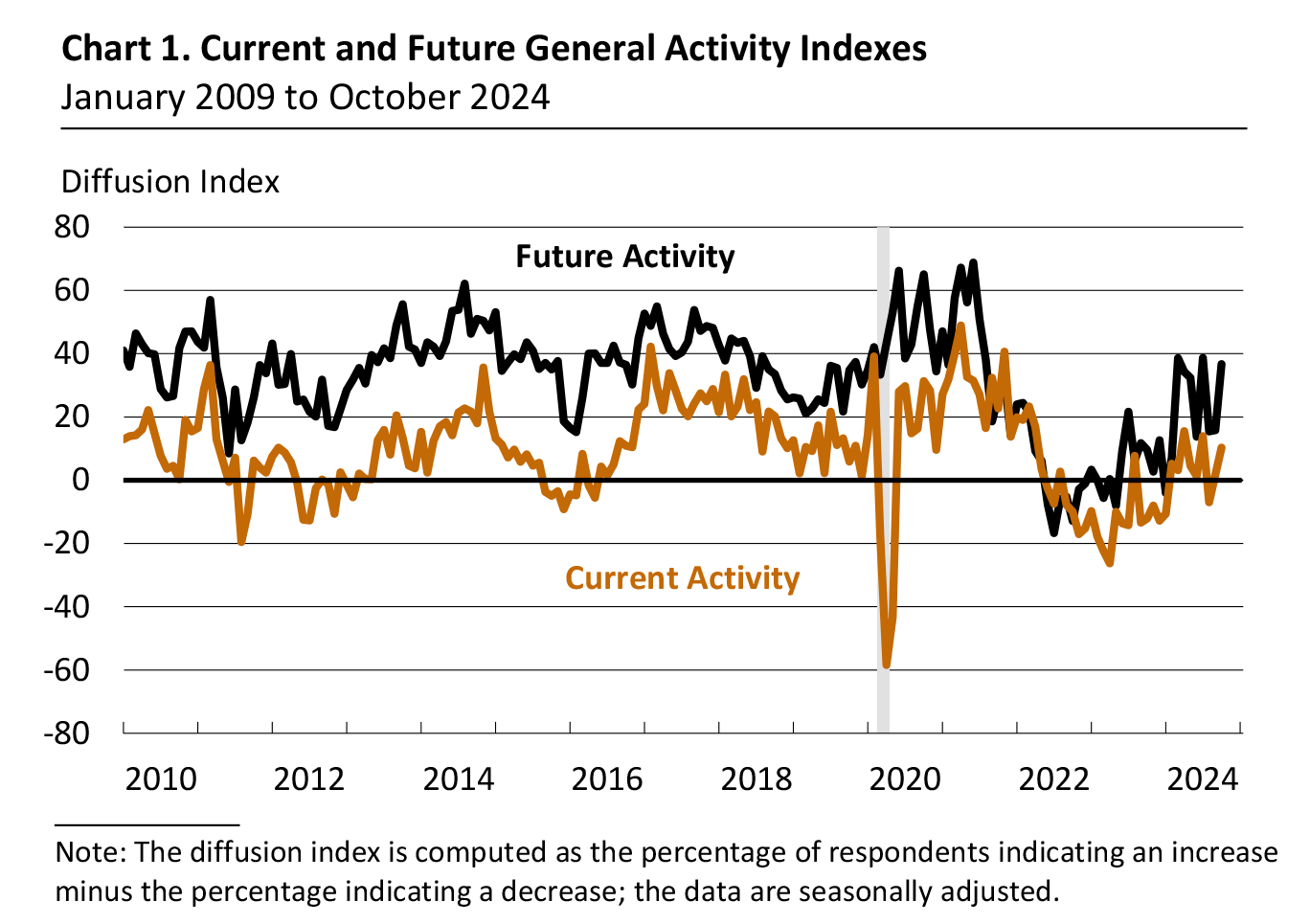

Most Current Indicators Improve

The diffusion index for current general activity rose from 1.7 to 10.3 in October, its second consecutive increase (see Chart 1). More than 24 percent of the firms reported increases in general activity this month, while 14 percent reported decreases; 57 percent reported no change. The indexes for new orders and shipments, which had turned negative last month, nearly recovered their declines from September. The new orders index climbed 16 points to 14.2, and the shipments index rose 22 points to 7.4.

The firms reported mostly steady employment as the employment index declined from 10.7 to -2.2. Most firms (76 percent) reported no change in employment levels, while the share reporting decreases (13 percent) narrowly exceeded the share reporting increases (11 percent). The average workweek index inched up from -13.6 to -11.8.

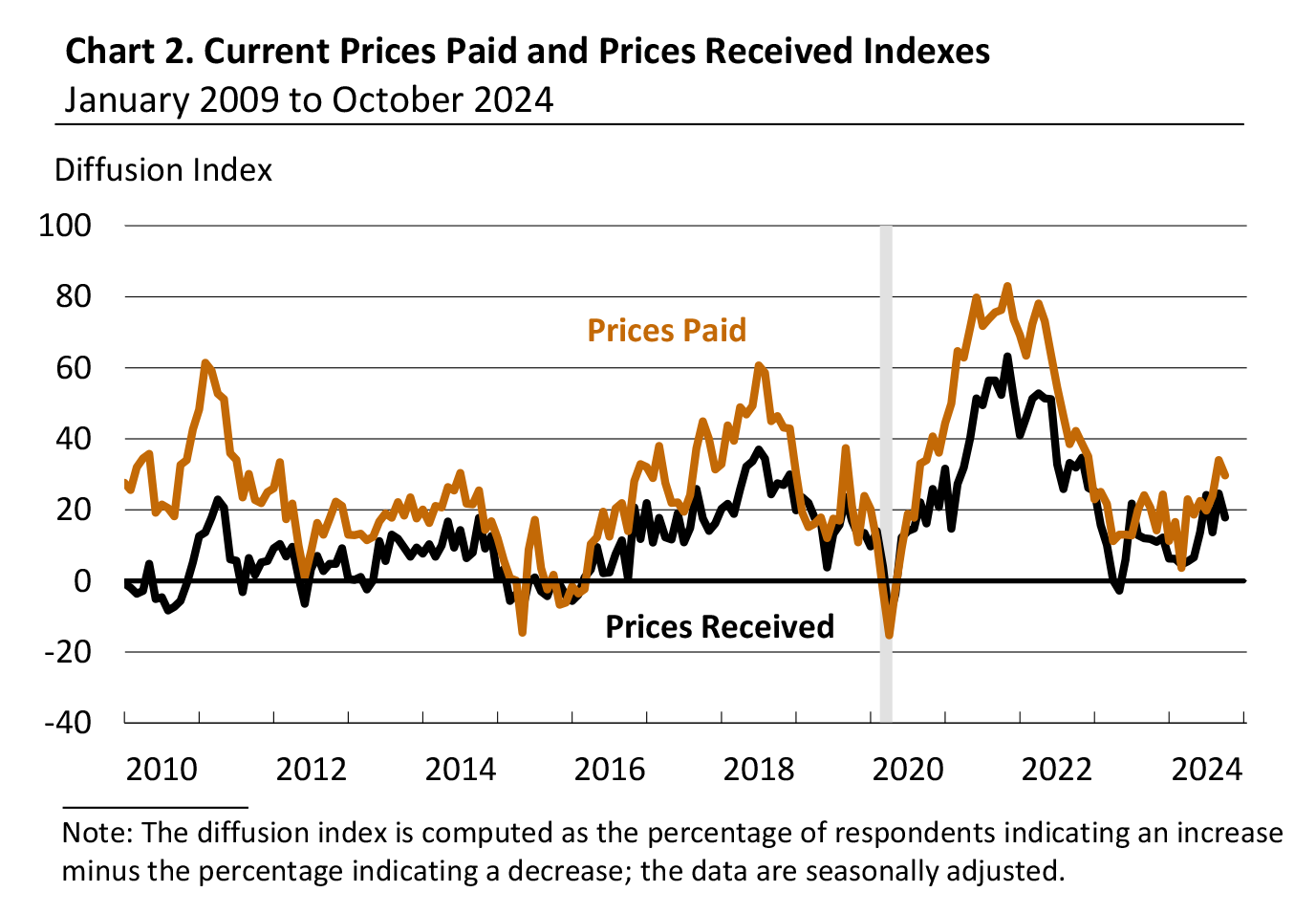

Firms Continue to Report Overall Price Increases

Both price indexes declined but remained positive. The prices paid index declined from 34.0 to 29.7 (see Chart 2). Nearly 35 percent of the firms reported increases in input prices, while 5 percent reported decreases; 60 percent of the firms reported no change. The current prices received index decreased 7 points to 17.9. Almost 22 percent of the firms reported increases in prices received for their own goods, 4 percent reported decreases, and 72 percent reported no change.

Firms Anticipate Higher Capital Expenditures Next Year

In this month’s special question, manufacturers were asked about their plans for different categories of capital expenditures next year. Almost 52 percent of the firms expect to increase total capital spending, compared with 21 percent that expect to decrease total spending; 27 percent expect total spending to stay the same. When this question was asked last year, the share of firms expecting to decrease spending slightly exceeded the share of firms expecting to increase spending (30 percent versus 24 percent). On balance, the firms expect higher capital expenditures next year for computer and related hardware, software, noncomputer equipment, and energy-saving investments, and lower expenditures on structure and other investments.

Firms Expect Growth over Next Six Months

The diffusion index for future general activity rose from 15.8 to 36.7 in October (see Chart 1). Over 47 percent of the firms expect increases in activity over the next six months (up from 39 percent last month), while 11 percent expect decreases (down from 23 percent); 34 percent expect steady conditions (up from 24 percent). The future new orders and shipments indexes rose to 40.1 points and 45.8 points, respectively, their highest readings since the spring. The firms continue to expect an overall increase in employment over the next six months, and the future employment index rose from 19.1 to 27.3, its highest reading since May 2022. Both future price indexes remained elevated, and none of the firms expect decreases in either. The future capital expenditures index remained elevated but ticked down 2 points to 23.5.

Summary

Responses to the October Manufacturing Business Outlook Survey suggest an overall increase in regional manufacturing activity this month. The indicators for current activity, new orders, and shipments were positive, and all rose from last month. On balance, the firms indicated mostly steady employment and continued to report increases in prices. The survey’s future indicators suggest more widespread expectations among the firms for growth over the next six months.

Special Question (October 2024)

| Comparing 2025 with 2024, do you expect capital expenditures to be higher, the same, or lower for each of the following categories? | ||||

|---|---|---|---|---|

|

Higher (% of reporters) |

Same (% of reporters) |

Lower (% of reporters) |

Diffusion Index |

|

| Software | 36.4 | 51.5 | 12.1 | 24.2 |

| Noncomputer equipment | 33.3 | 48.5 | 18.2 | 15.2 |

| Energy-saving investments | 19.4 | 66.7 | 9.7 | 9.7 |

| Computer and related hardware | 36.4 | 57.6 | 6.1 | 30.3 |

| Structure | 12.1 | 66.7 | 16.1 | -4.0 |

| Other | 0.0 | 88.9 | 11.1 | -11.1 |

| Total capital spending | 51.5 | 27.3 | 21.2 | 30.3 |

Return to the main page for the Manufacturing Business Outlook Survey.