February 2023 Nonmanufacturing Business Outlook Survey

Note: Survey responses were collected from February 6 to February 16.

Nonmanufacturing business activity continued to expand overall this month, according to the firms responding to the February Nonmanufacturing Business Outlook Survey. The index for general activity at the firm level increased, and the indexes for new orders and sales/revenues remained positive but declined. The indexes for full- and part-time employment decreased this month but remained positive. The prices paid and prices received indexes both rose this month. The respondents continue to expect growth over the next six months.

Current Indicators Remain Positive

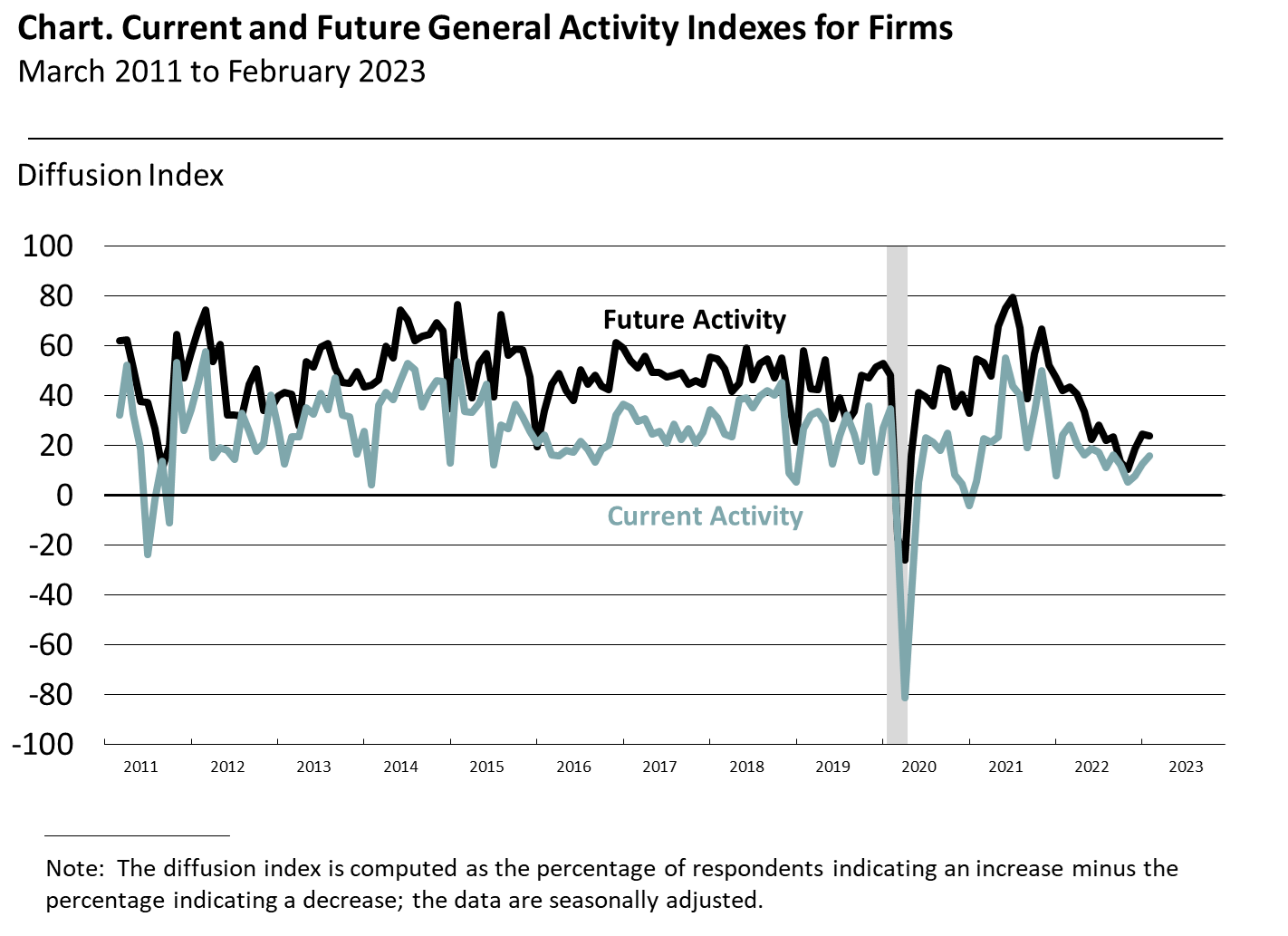

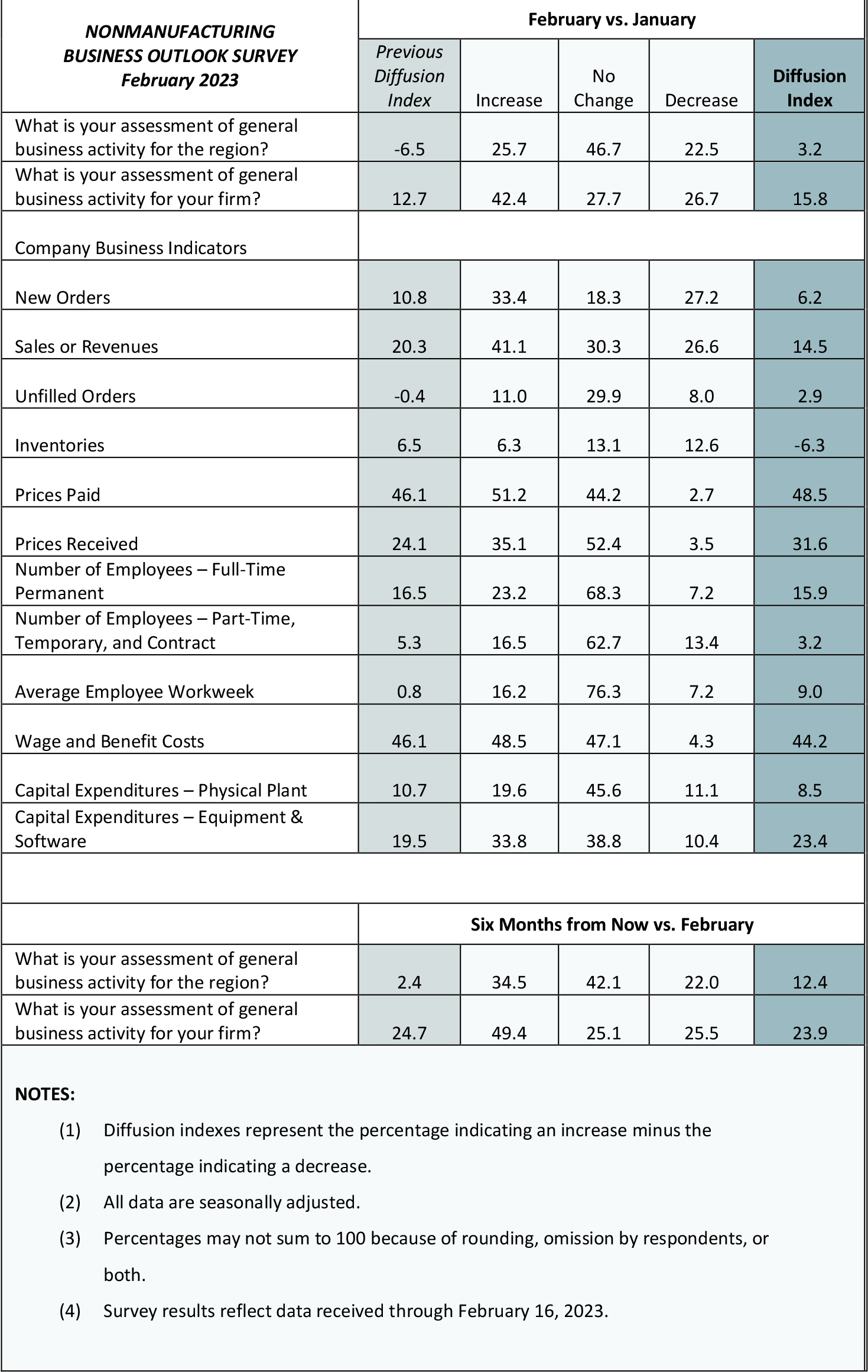

The diffusion index for current general activity at the firm level rose 3 points to 15.8, its third consecutive increase since December (see Chart). The share of firms reporting increases (42 percent) exceeded the share reporting decreases (27 percent). The new orders index fell 5 points to 6.2 this month. More than 33 percent of the firms reported increases in new orders (up from 31 percent), while 27 percent reported decreases (up from 20 percent). After a sharp increase last month, the sales/revenues index decreased from 20.3 to 14.5. Over 41 percent of the firms reported increases in sales/revenues, while 27 percent reported decreases. The current regional activity index rose to 3.2 in February, its first positive reading since July.

Firms Report Overall Employment Increases

The firms reported overall increases in both full- and part-time employment. The full-time employment index edged down 1 point to 15.9. The share of firms reporting increases in full-time employment (23 percent) exceeded the share reporting decreases (7 percent); most firms (68 percent) reported no change. The part-time employment index declined 2 points to 3.2. Most firms (63 percent) reported steady part-time employment, while 17 percent of the firms reported increases and 13 percent reported decreases. The average workweek index increased 8 points to 9.0.

Firms Continue to Report Price Increases

Price indicator readings suggest widespread increases in prices for inputs and the firms’ own goods and services, and both indexes increased this month. The prices paid index – which has declined more than 30 points since October – increased 2 points to 48.5 in February. More than 51 percent of the firms reported increases in input prices, while 3 percent reported decreases; 44 percent reported stable prices. Regarding prices for the firms’ own goods and services, the prices received index rose 8 points to 31.6 this month. More than 35 percent of the firms reported higher prices, 4 percent reported lower prices, and 52 percent reported no change.

Firms Expect Lower Increases in Prices from Last Quarter

In this month’s special questions, the firms were asked to forecast the changes in prices of their own products and for U.S. consumers over the next four quarters. Regarding their own prices, the firms’ median forecast was for an increase of 3.5 percent, down from 4.0 percent when the question was last asked in November. The firms’ reported own price change over the past year was 3.0 percent. The firms expect their employee compensation costs (wages plus benefits on a per employee basis) to rise 5.0 percent over the next four quarters, unchanged from November. When asked about the rate of inflation for U.S. consumers over the next year, the firms’ median forecast was 5.0 percent, down from 6.0 percent in November. The firms’ median forecast for the long-run (10-year average) inflation rate was 4.0 percent, down from 5.0 percent in November.

Future Indicators Remain Positive

The future activity indexes suggest firms expect growth at their own companies and in the region over the next six months. The diffusion index for future activity at the firm level ticked down 1 point to 23.9 this month (see Chart). The share of firms expecting increases (49 percent) exceeded the share expecting decreases (26 percent). The future regional activity index increased from 2.4 to 12.4 this month.

Summary

Responses to this month’s Nonmanufacturing Business Outlook Survey suggest continued expansion in nonmanufacturing activity in the region. The indicator for firm-level general activity increased, while the indexes for sales/revenues and new orders both remained positive but decreased. The indexes for both full- and part-time employment continue to reflect overall increases in employment. Both price indexes increased this month. Overall, the respondents continue to expect growth over the next six months.

Special Questions (February 2023)

| Please list the annual percent change with respect to the following: | ||

|---|---|---|

|

|

Current |

Previous (Nov. 2022) |

| For your firm: | ||

| Forecast for next year (2023Q1–2024Q1) | ||

| 1. Prices your firm will receive (for its own goods and services sold). | 3.5 | 4.0 |

| 2. Compensation your firm will pay per employee (for wages and benefits). | 5.0 | 5.0 |

| Last year's price change (2022Q1–2023Q1) | ||

| 3. Prices your firm did receive (for its own goods and services sold) over the last year. | 3.0 | 3.8 |

| For U.S. consumers: | ||

| 4. Prices U.S. consumers will pay for goods and services over the next year. | 5.0 | 6.0 |

| 5. Prices U.S. consumers will pay for goods and services over the next 10 years (2023–2032). | 4.0 | 5.0 |

| The numbers represent medians of the individual forecasts (percent changes). For question 5, firms reported a 10-year annual-average change. | ||

Summary of Returns (February 2023)

Return to the main page for the Nonmanufacturing Business Outlook Survey.