Large Bank Credit Card and Mortgage Data 2026 Q1 Narrative

Q1 2026 Insights Report

by Lauren Berlin & Jacob Sloan

Published: July 13, 2026

Credit Card Borrowers Continue to Spend, While Mortgage Refinancing Surge Shows Pent-Up Demand

Large bank credit card borrowers demonstrated financial resilience in the first quarter of 2026, continuing to spend while nonetheless managing their revolving credit card debt. With credit card delinquency rates stabilized, large banks have been easing card underwriting standards slightly with an eye toward portfolio growth.

Rate-sensitive mortgage borrowers took advantage of a temporary easing of interest rates in the first quarter, driving growth in large bank mortgage refinances. Meanwhile, new borrowers have increasingly opted for adjustable-rate mortgages (ARMs) to secure lower initial monthly payments, as mortgage rates and home prices are still high by historical standards. Large bank mortgage credit performance continues to show strength, with delinquency rates near historical lows.

For additional questions or feedback about these data and this report, please email Phil.LargeBankData@phil.frb.org.

Credit Card Utilization Eases Even as Consumers Continue to Spend

Total credit card balances at the large banks stood at $948.7 billion as of the first quarter of 2026. This was an increase of 3.2 percent relative to one year earlier, slightly below the rate of inflation and moderately lower than the average annual growth rate of 3.8 percent across the entire time series. Total credit card commitments rose 4.2 percent over the same period, marking the fifth consecutive quarter in which year-over-year growth in commitments outpaced that of balances; as a result, the overall rate of credit utilization is now at its lowest level in three years, at 19.1 percent.1

Given subdued consumer sentiment and still-elevated interest rates on credit card balances, one might assume that the softening in credit utilization results from a moderation or an outright pullback in new spending. However, purchase volume during the first quarter was 6.4 percent higher than a year earlier. Instead, the declining utilization rate reflects muted growth in revolving balances in recent years. Revolving balances have risen more slowly than inflation in recent quarters; in real terms, they were at their lowest level since mid-2023 (Figure 1) and in fact were lower than just before the beginning of the pandemic.

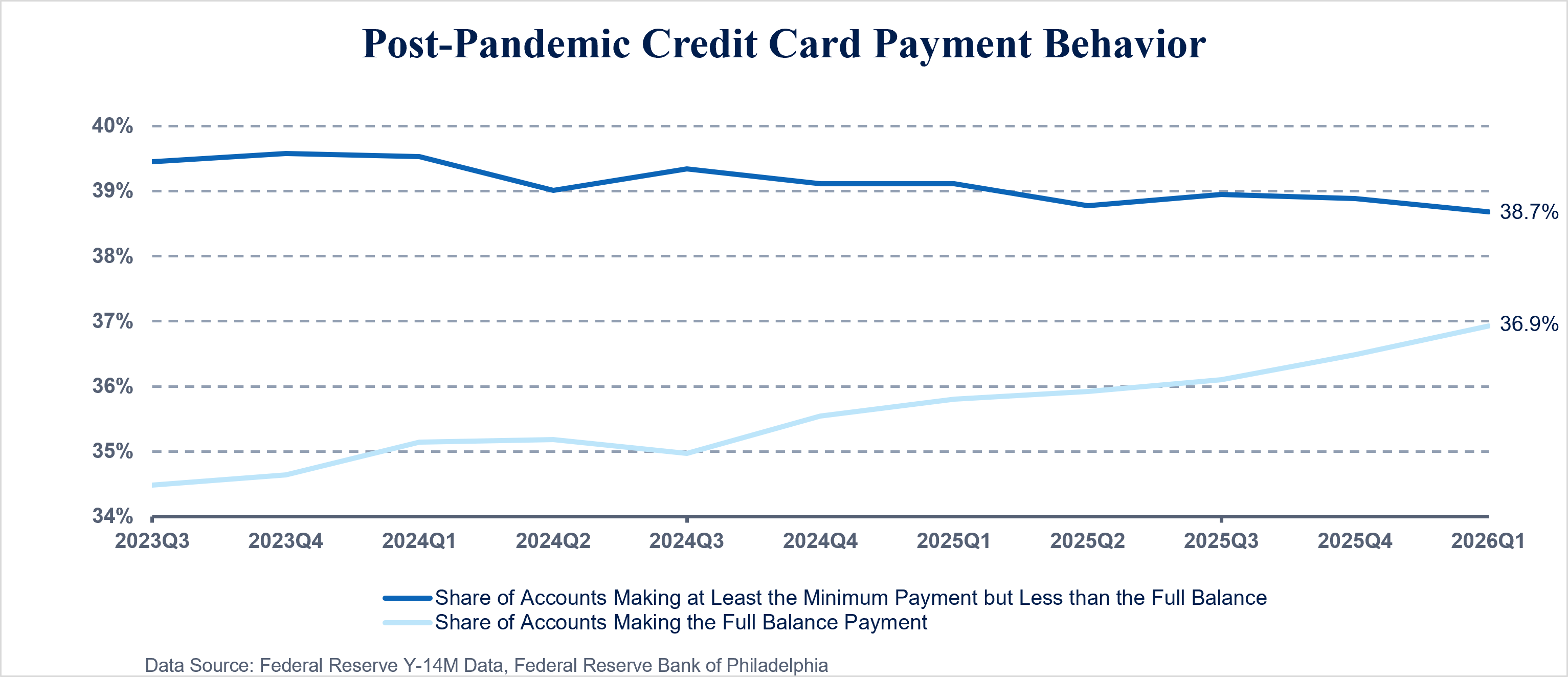

Card Payment Behavior Patterns Evolve

The subdued growth in revolving balances in recent years reflects shifting payment behavior: The share of credit card accounts paying their balance in full reached an all-time series high in the first quarter of 2026. By contrast, the combined share of accounts paying either the minimum due or more than the minimum but less than the full amount has declined slightly on a yearly basis in seven consecutive quarters (Figure 2).2 This suggests that cardholders with the ability to do so are prioritizing paying in full to avoid interest charges rather than carrying partial balances. With the average interest rate on general-purpose cards currently at 24.0 percent (up from a historical average of 18.2 percent before the most recent rate hike cycle in 2022), the cost of carrying a balance has noticeably risen, likely influencing these payment patterns.

Another encouraging development is the continued decline in credit card delinquency rates, which over the past two years have gradually but steadily retreated from series peaks. The proportion of outstanding card balances 30+ days past due stands at 3.3 percent, down year over year for the sixth straight quarter. (The net charge-off rate, or the share of balances written off as a loss, typically lags delinquency trends and has fallen in four consecutive quarters when compared with a year earlier.) However, even with this improvement, card delinquency rates remain above series historical norms.

Increased Card Originations Signal Shift from Credit Tightening

The dollar volume of credit card originations rose by a robust 8.7 percent year over year in the first quarter of 2026 to $105.5 billion. The increase in the number of new accounts was even more pronounced, at 11.2 percent annual growth. This was the latest indication that large banks have shifted away from the credit tightening evident in 2023 and 2024; with credit card delinquency rates having stabilized, banks have been easing underwriting standards slightly in pursuit of portfolio growth.

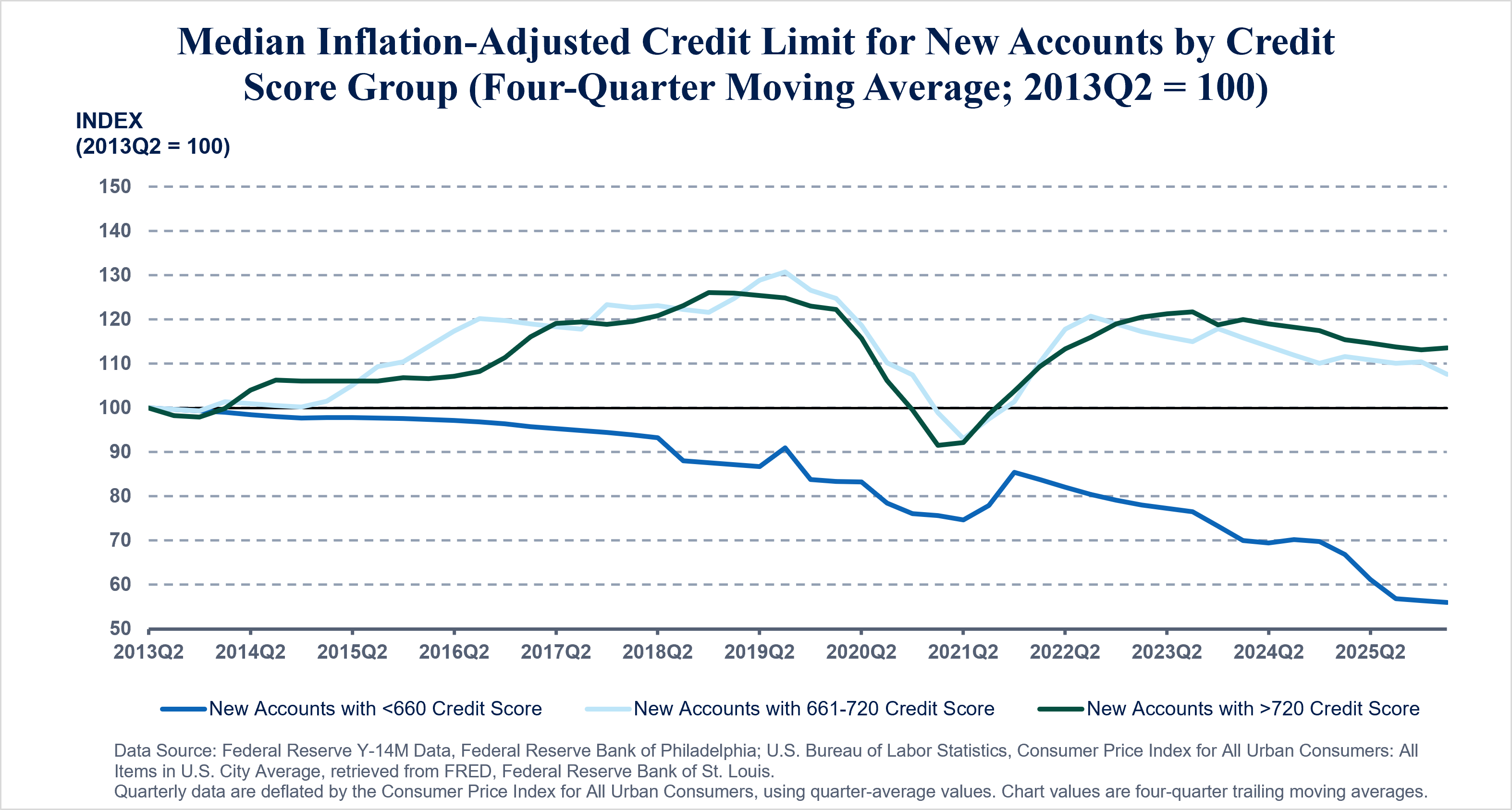

As part of this strategy, large banks are showing increased appetite for lending to marginal credit card applicants. The 10th percentile credit score for new accounts dropped to 619 in the first quarter, the lowest value in more than four years, down from 628 in the previous quarter and 632 a year earlier. More broadly, consumers with credit scores below 660 represented nearly one in five new accounts (19.2 percent), the highest share in nearly three years.

Although banks appear more willing to extend accounts to riskier borrowers, they are keeping such borrowers on a relatively short leash. The sub-660 cohort’s share of new commitments remains low by historical standards at 4.0 percent. The median credit limit for new accounts within this group was just $500, down from $700 a decade earlier, even as the corresponding figure for borrowers with credit scores above 720 rose 53 percent over the same period. As Figure 3 shows, the long-term decline in credit limits for the low-score group is even more dramatic when adjusted for inflation.

First-Lien Mortgage Affordability Concerns Drive Growth in Refinance Activity and ARM Originations

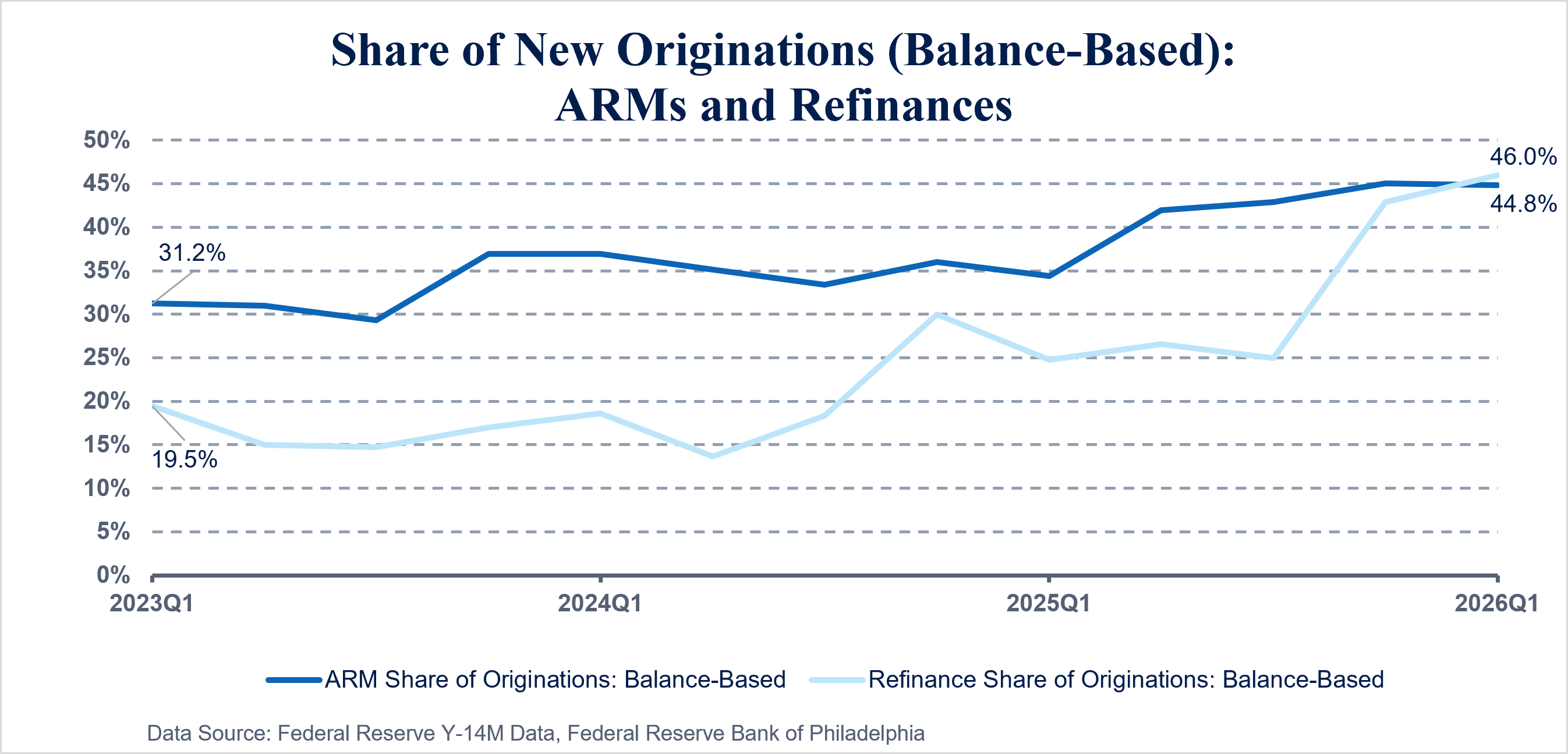

Total first-lien mortgage balances for large banks reached $1.47 trillion in the first quarter of 2026, marking the fourth consecutive quarter of modest growth. Mortgage originations totaled $73.32 billion, up 45 percent year over year but still historically low for large banks. Declining interest rates drove the recent consumer demand as the average 30-year fixed rate at origination for prime (>=740 score) large bank borrowers reached a three-year low of 6.12 percent in the first quarter of 2026. Borrowers took advantage of recent rate relief to reduce monthly payments or tap into existing home equity through refinances. Originations for cash-out refinances and rate/term refinances increased by roughly 52 percent and 300 percent year over year, respectively. When combined, refinances accounted for 46 percent of total new large bank originations in the first quarter of 2026, compared with just 19 percent three years ago (Figure 4). The increased demand for refinances may temper in the coming quarter as rates climbed again.

Although mortgage rates temporarily dipped in the first quarter, both rates and home prices remain historically high and continue to constrain affordability. The median new loan size ($361,888) for large banks, which increased by 10 percent year over year, underscores the high costs facing borrowers. New borrowers have increasingly opted for ARMs, as opposed to fixed-rate mortgages, to secure lower initial monthly payments during the introductory fixed-rate period, often three, five, seven, or 10 years. Large bank ARM originations have risen 89 percent in the past year, compared with only 22 percent for fixed-rate originations, and ARMs accounted for 45 percent of total new originations (Figure 4) in the first quarter of 2026. The U.S. mortgage market has also seen an increase in the share of borrowers opting for ARMs, although ARMs remain less prevalent in the broader market, according to data from Intercontinental Exchange (ICE).

Large bank first-lien mortgage credit performance continues to show strength, with delinquency rates near historical lows. This is in contrast to the broader U.S. market, which saw an increase in serious delinquencies (90+ days past due) year over year, driven largely by Federal Housing Administration (FHA) loans.3 These loans, which are typically designed to help first-time buyers and borrowers with limited savings or lower credit scores, are not represented in the large bank data. For the large bank portfolio, the share of accounts 30+ days past due decreased to 2.43 percent in the first quarter of the year from 2.49 percent at 2025 year-end, while serious delinquencies (90+ days past due) remained at just 0.85 percent. This strong performance reflects substantial home equity positions built through significant price appreciation following the pandemic. Also benefiting credit performance are the stringent post-Great Recession underwriting standards that have contributed to high borrower credit quality. The median current credit score has held at its series high of 793 for three consecutive quarters.

- Disclaimer: The views expressed in this report are solely those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Philadelphia or the Federal Reserve System.