Research is a key part of the Federal Reserve Bank of Philadelphia’s work to support a strong and stable economy. From new innovations to emerging economic trends, our researchers examine an array of topics to provide insights about the economic impact on consumers. Daniel Sanches, an economic advisor and economist at the Philadelphia Fed, has focused on banking and financial markets since he joined the Bank in 2010. Most recently, his research interest has tracked the emergence of digital currency as well as the market effects — both positive and negative — of central bank digital currency (CBDC) on countries currently exploring this possibility. We spoke to Daniel about his research, the new Digital Currency Center, and what lies ahead.

advisor and economist who has

been studying financial markets

and digital currency.

Q: Tell us what first interested you in the financial sector?

DS: My interest in money actually started in middle school when I was growing up in Brazil in the 1980s. The average inflation rate was highly variable and reached about 50 percent to 60 percent per month occasionally, so you quickly learned about money to survive. Those who had cash had to spend it quickly and plan their expenses in advance every month. But I noticed that some people had access to the banking system and could deposit money and get interest overnight. Not everyone had that access though. Then, in 1994, a successful currency reform in Brazil reduced inflation to less than 5 percent annually. The value of cash assets stabilized, and people had more purchasing power and more control over their finances. My interest in economics grew from there.

Q: Your paper on “Banking Panics and Output Dynamics” explored outcomes from government policy responses in a banking crisis. What similarities do you see today, especially since we just experienced some banking unrest?

DS: Nobel Prize-winning author Milton Friedman and Anna J. Schwartz published A Monetary History of the United States, 1867–1960 in 1963, which investigated the effects of banking panics on real economic activity. They pointed out that a banking crisis impairs not only the banking system’s ability to extend credit to households and firms but also the purchasing power of consumers, who have part of their wealth deposited in the banking system. When many people withdraw their deposits from the banking system during a panic, banks must contract their loan portfolios, which has an impact on real activity. That’s the traditional channel. But the authors proposed a second channel because bank liability also serves as money. If bank liability holders, or bank depositors, suffer losses because banks are failing, it also influences their spending decisions because their purchasing power declines, so they can’t buy as much as before. So, my paper formalizes this theory by using a state-of-the-art dynamic model that Friedman and Schwartz didn’t have at the time.

There’s also one more step when there is a banking panic, which we saw recently. Although corporations fail, you don't usually see governments intervene on their behalf. But you do see governments intervene with banks. Why? Because policymakers understand the effects of a banking crisis on aggregate consumption and investment.

Although corporations fail, you don’t usually see governments intervene on their behalf. But you do see governments intervene with banks. Why? Because policymakers understand the effects of a banking crisis on aggregate consumption and investment.

My paper takes that intervention into account. In my model, the depositors anticipate that the government will end up intervening at some point during a banking crisis to preserve the value of banking assets and the purchasing power of consumers. This anticipation by bank depositors, in fact, influences their decision to run on the banking system and prematurely withdraw their deposits. Taking this rational response by depositors into account, I find that, under certain circumstances, a banking panic may not occur at all. When it does happen, government intervention tends to smooth out fluctuations in aggregate consumption and investment.

The recent banking turmoil did not involve the whole banking system, which is a key difference from the episodes that Friedman and Schwartz studied. The banks that failed this year had very specific characteristics in their business models that led depositors to suddenly withdraw their deposits. Most important, those developments occurred in a segment of the banking system and did not result in a liquidity crisis.

Q: We hear about cryptocurrency, digital currency, bitcoin, and stablecoin. How are they connected?

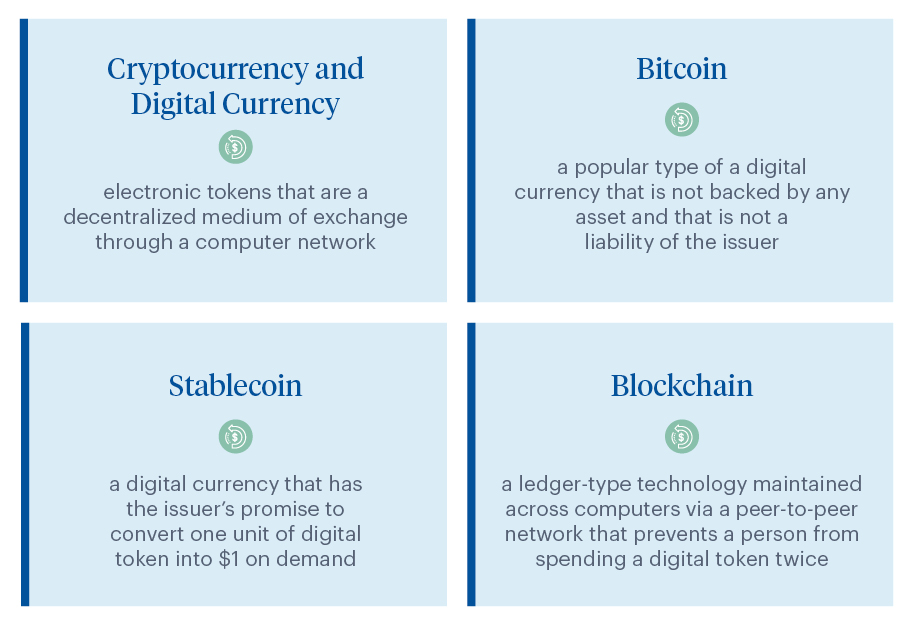

DS: Basically, cryptocurrency and digital currency are quite similar. They are all electronic tokens. Bitcoin is a type of a digital currency.

Digital tokens, such as bitcoins, are not easily reproducible, but you have to find a way to issue tokens so people can’t double-spend. And one problem with creating any type of money is counterfeiting. If you have a Federal Reserve note, for example, you want to make sure that people don’t copy the technology and make their own counterfeit money, which is illegal in the United States. Digital tokens solve that problem in a different way by using a blockchain, which is a ledger-type technology maintained across computers linked via a peer-to-peer network. When used in a specific way, the blockchain technology allows network participants to create digital tokens that cannot be counterfeited and that preserve the anonymity of token holders.

Now, a stablecoin is different from cryptocurrencies such as Bitcoin and Tether and is similar to bank deposits. At a bank, you have the right to claim the value of your deposit because there are rules for withdrawing money. There is that implicit promise, a contractual obligation involved.

And banks are regulated by federal and state authorities. Like bank deposits, a stablecoin involves a contractual obligation in which stablecoin issuers promise to convert each unit of their token into $1. Unlike bank deposits, stablecoins are not regulated, and the way they report the assets backing their liabilities is very different from that of banks.

(Listing may shift over time.)

With the global crypto market cap totals now at about a trillion dollars, the five largest digital currency traders now include two that deal in stablecoin and three in cryptocurrency. Tether and USD Coin are stablecoins; Bitcoin, Ethereum, and BNB are cryptocurrencies.

Q: You’ve done research on cryptocurrencies and CBDCs. What are some key takeaways?

DS: In 2016, I coauthored an article on cryptocurrencies with Jesús Fernández-Villaverde from the University of Pennsylvania. We constructed a model for our experiment: We assumed a central bank did not exist, and all money was issued by private firms. The money issued was not necessarily an obligation for the firm, which is similar to a bitcoin. Specifically, we considered a scenario in which many small issuers compete for customers in the money market. And we asked whether this financial/monetary system would be stable for households and businesses. It’s a question that Nobel Prize winner [Friedrich von] Hayek also posed in 1976 when inflation was high.

We discovered in our analysis that getting a stable monetary system isn’t easy because so much depends on the technology used to issue tokens. With most of the common technological features, you don’t get stable value, which means there would be perpetual inflation. Because of the very low barrier to entry, the issuers wouldn’t be large firms. Basically, anyone with a set of powerful computers could issue these digital tokens. They wouldn’t internalize the effects of issuing tokens on the aggregate money supply, so they could keep issuing digital tokens, causing monetary instability and variable inflation rates.

Q: And what about CBDCs?

DS: Virtually all central banks around the globe are studying the possibility of issuing an electronic version of their physical currencies and the potential benefits and risks it can bring to the monetary and financial system. A central bank digital currency is a version of central bank money that can be used as a means of payment in a network of computers. The specific form it can take varies across different studies, but one commonly discussed form is through a specific type of segregated account provided by select financial institutions under direct supervision from the central bank. One aspect of a CBDC that concerns many economists — me included — is the effect it can have on other means of payments issued by private financial institutions, such as commercial banks.

One aspect of a CBDC that concerns many economists — me included — is the effect it can have on other means of payments issued by private financial institutions, such as commercial banks.

Commercial banks issue deposits to households and firms and use part of the proceeds from deposits to make loans to households and firms. Not only do banks issue a valuable means of payment to households and firms, but they also allocate credit across different sectors of the economy. Introducing a CBDC is likely to cause a shift of funds, by households and firms, out of deposits because a CBDC is designed to be a safe form of payment that can be transferred electronically and instantaneously. Todd Keister (from Rutgers University) and I explore this scenario in a recent paper. We find that creating an interest-bearing CBDC usually benefits households and firms. But the central bank must tread carefully when making its decision to issue a CBDC. We have also identified scenarios in which the contractual frictions in credit markets can be sufficiently severe to result in an inefficiently low amount of intermediation and credit creation even in the absence of a CBDC. In this case, issuing a CBDC can exacerbate this problem, leading to lower welfare in the economy.

Q: The Bank recently launched the Digital Currency Center on the Philadelphia Fed website. What can we find there?

DS: The Digital Currency Center site is a new hub on our website that provides links to presentations on digital currency, summaries of conferences we have hosted, research publications, and other resources. I had already been researching cryptocurrency for the Research Department when we organized our first conference on digital currency in 2020 so researchers and experts could discuss the topic. Since then, we’ve added another economist to our team, Joseph Abadi, and hosted another conference in 2021. Our third is planned for this fall. This year’s agenda will involve research on stablecoins, digitized tokens, and new ways of financing firms. There seems to be much more interest in how start-ups can raise capital.

When I first presented a seminar on digital currency, economists wanted to know why this topic was important. I explained that thousands of innovations were dismissed as being useless initially but ended up being valuable to society. It is hard to predict which inventions will turn out to be useful in the future. The same is true for digital currencies. Although the benefits of digital currencies are not clear now, it is difficult to imagine that our money will not be totally digital in the future.

Q: What research topics will you be tackling next?

DS: I’ll continue my research on digital currency. I think stablecoins will continue to grow, probably more internationally than they are now. But for international commerce, the question is whether digital currency will be more useful for institutional investors to improve the flow of assets across borders.

I’m also looking at the future of banks. Banks have a franchise value in their capacity to grow over time because of regulations. While there are restrictions on bank activities, banks are protected from competition in a sense. You have deposit insurance and other federal guarantees that make businesses safe for the public, even though there are restrictions on investments and liquid assets.

One of the reasons we have regulations is to prevent recurrent banking failures. It's not always clear what the new technologies are capable of, but fraud is likely to be a problem. It doesn't mean technology is bad, it's just that bad players see an opportunity to take advantage of the technology. People want to find an easy way to make money with anything, not just cryptocurrency.

- The views expressed here are solely those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Philadelphia or the Federal Reserve System. This interview has been edited for clarity and length.