Fintech: At the Intersection of Technology and Financial Services

Julapa Jagtiani leads the annual fintech

conference at the Philadelphia Fed.

The Federal Reserve Bank of Philadelphia has become a trailblazer in understanding the evolving world of fintech. Leading the effort is Julapa Jagtiani, senior economic advisor and economist in the Supervision, Regulation, and Credit Department, who guides the team that brings fintech experts together for our annual fintech conference. The Bank’s Seventh Annual Fintech Conference in September opened the doors to 157 in-person attendees and more than 1,400 online participants to discuss fintech issues and the latest trends. Here, Jagtiani shares some history of the conference and what lies ahead.

Q: How and why did you first decide to launch a conference on fintech in 2016?

JJ: It all started when I was writing and reviewing sources for a journal article on credit access to small businesses in 2015. I noticed that banks had been making fewer loans to small businesses. This was especially true for small community banks, which serve as a primary source of credit for local small businesses through relationship lending. I saw that larger banks were taking market share away from smaller banks. And the overall banking industry had been losing market share to nonbank small business lenders, including fintech lenders.

The more I explored the data, the more I realized that through technology it was no longer necessary for lenders and borrowers to be in proximity or to have an established lending relationship to do business. In a digital economy, information is collected about all of us all the time, and a fintech lender from far away could have a holistic view of our financial situation as well as a small bank in our own hometown. I realized that crowdfunding and peer-to-peer (P2P) lending, which leverage alternative, or nontraditional, data sources, have the potential to disrupt traditional lenders.

Q: How did the financial services industry respond to the Bank’s first fintech conference?

JJ: Our first fintech conference in 2016 was well received. Most of the sessions were presentations of research papers on various fintech-related issues, such as fintech lending, the use of alternative data and artificial intelligence/machine learning (AI/ML) in credit decisions, and data aggregation. We partnered with an academic finance/economics journal to publish selected papers that were presented at the conference. All of the papers went through the referee process, but these papers were published in a special journal issue where I was a guest coeditor, along with our organizing partners from the Wharton School of the University of Pennsylvania. For three consecutive years, we had special issues on fintech through our partnerships with the Journal of Economics and Business and the Journal of Financial Services Research. The selected papers published in these special issues have been widely cited.

The agendas for the conferences continued to evolve, following trends we observed as well as the new types of products and services offered by fintech platforms. We kept adding more policy sessions and industry practitioner sessions. That way, we could connect all the relevant stakeholders at the same event: academic researchers, fintech industry practitioners, bankers, lawyers, bank supervisors, policymakers, and others.

Currently, world-renowned researchers still participate in our annual fintech conference, but instead of presenting a specific paper, they apply their knowledge and expertise — to discuss policy questions and to debate with other qualified experts who may hold opposite viewpoints, based on their research or industry experience.

Q: Is it easier to get fintech companies to participate in the Bank’s fintech conference today than in the early days?

JJ: It has never been easier to get fintech companies to participate in our fintech conferences, for a few good reasons. The quality of the speakers has become better over time, and we keep raising our own bar.

Our agendas have expanded to include experts who (understand fintech but) are fintech skeptics. Over the years, fintech experts have learned that our fintech conference is a “safe place” where they can speak up and share their thoughts. We are all trying to learn from each other, working together to come up with potential solutions that would make things better for everyone. Speakers talk about their ideologies and beliefs, rather than being on stage to promote their products or services.

Q: What needs are fintech firms fulfilling in today’s financial services landscape?

JJ: Fintech is definitely fulfilling more than a few needs in today’s financial services landscape. For instance, a 2021 FDIC report confirmed that 4.5 percent (5.9 million) of American households are unbanked, meaning no one in the household has an account at a bank or credit union. These unbanked consumers may need to rely on nonbanking alternatives such as check cashing services, payday lenders, or others, which can be more expensive for the consumer. In addition, this reliance on cash can limit the ability to send money or pay bills online; some consumers cannot easily send money to their loved ones who may live far away because they rely on cash as a means of payment. In those cases, fintech can help. Some fintech firms offer banking services to their customers directly or through partnership with a bank. Plus, some fintechs do not charge overdrafts or other fees, and some give customers faster access to their paychecks.

In terms of credit access, the Consumer Financial Protection Bureau2 estimated that about 26 million Americans are credit invisible, meaning that they don’t have a credit file with any of the three major credit bureaus. Another 19 million are credit unscorable, which means they may have a credit file, but they have a credit history that is too thin or out-of-date to be assigned a credit score, leaving them unable to access credit. Fintech firms can also help these consumers by assigning a score based on their alternative data. Fintechs can identify the invisible prime borrowers and grant them credit at a fair price, often much lower than what they could get from traditional lenders.

Q: Where do you think fintech is likely to venture next?

JJ: The term fintech is very broad now. It’s not just about P2P lending anymore. Fintech now includes blockchain; cloud computing; fintech partnerships; cryptocurrencies; real-time payments; buy now, pay later (BNPL); central bank digital currency (CBDC); decentralized finance (DeFi); quantum computing; and much more.

Many fintech firms have become banks through mergers and acquisitions. On Deck, SoFi, Kabbage, and LendingClub are examples of that. Banks have also become more technologically focused over the years, and many small banks are getting access to today’s technology through partnerships with fintech firms. Some large banks are building their own technology platform internally, while others simply acquire existing fintech firms.

But it’s not only banks. Financial services firms have also been acquiring fintech firms. Intuit acquired Credit Karma, Mastercard acquired Finicity, Square acquired Afterpay, and the list goes on.

The dividing line between fintech and traditional financial firms has become blurred over the years, and this is likely to continue. Traditional firms need to access technology to compete effectively, while fintech firms need to access a larger customer base and to garner consumer trust, which they could more easily do if they are part of a traditional firm. That is why we are seeing a lot of mergers and acquisitions. The entire financial system is adapting and evolving. It’s a long journey that involves both unbundling and bundling of financial products and services.

- The views expressed here are those of Julapa Jagtiani and do not necessarily reflect those of anyone else at the Federal Reserve Bank of Philadelphia or the Federal Reserve System. Some portions of this interview have been edited for space.

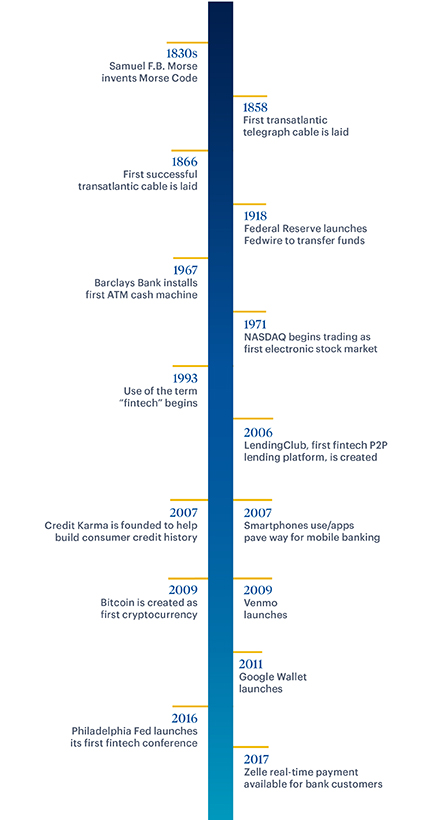

- Timeline comprises data from “The Evolution of Fintech: A New Post-Crisis Paradigm,“ by R. Buckley, D. W. Arner, and J. N. Barberis (January 2016); “Fintech: The History and Future of Financial Technology,” The Payments Association (October 2020), and additional research by Philadelphia Fed staff.

- “CFPB Explores Impact on Alternative Data on Credit Access for Consumers Who Are Credit Invisible,” Consumer Financial Protection Bureau, February 16, 2017.