September 2021 Manufacturing Business Outlook Survey

Note: Survey responses were collected from September 7 to September 13.

Manufacturing activity in the region continued to expand this month, according to the firms responding to the September Manufacturing Business Outlook Survey. The survey’s indicators for general activity and shipments improved, but the new orders and employment indexes softened somewhat. Both price indexes remained elevated. The survey’s future general activity and new orders indexes continued to moderate, but the surveyed firms remained generally optimistic about growth over the next six months.

Current Indicators Remain Elevated

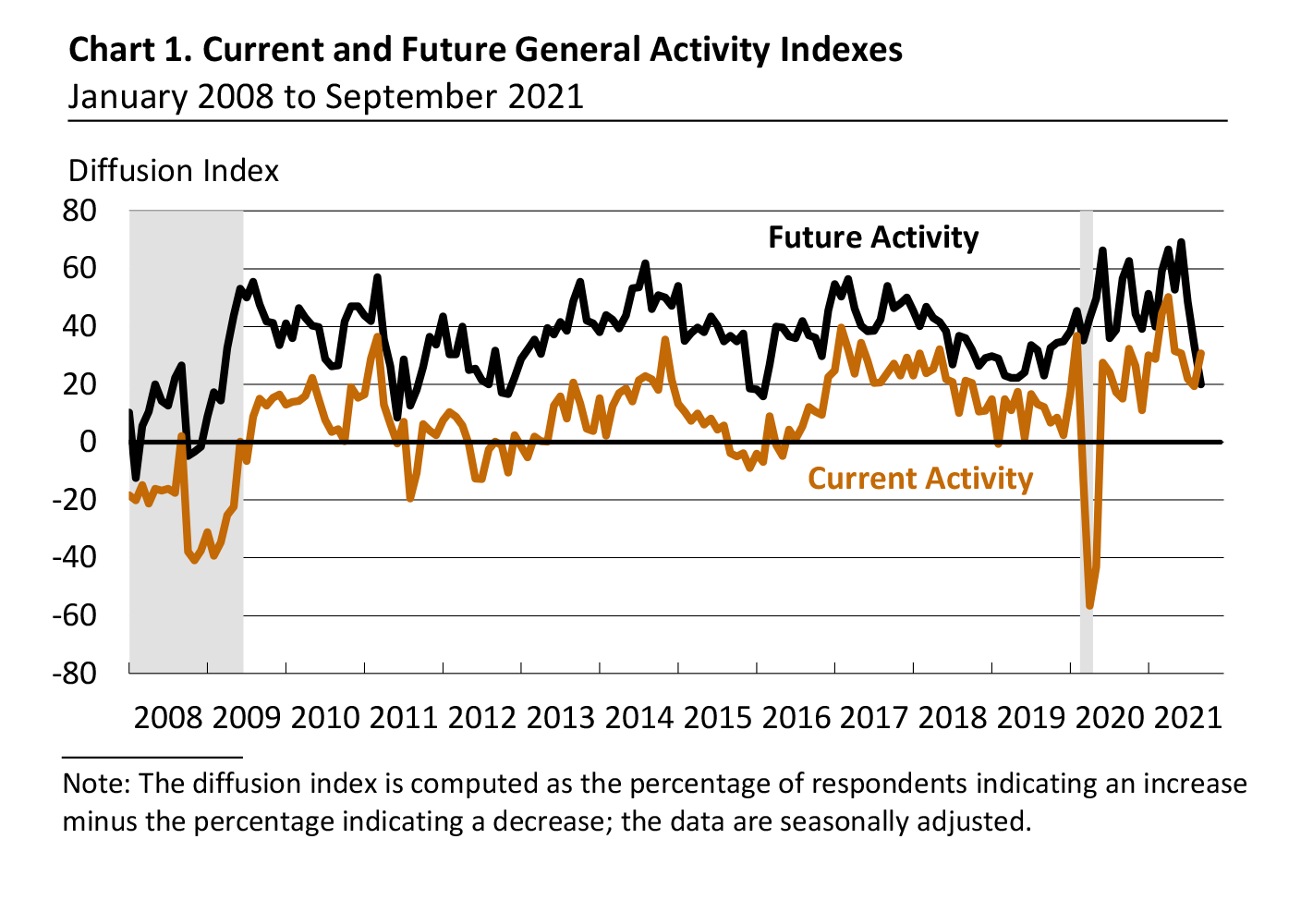

The diffusion index for current general activity rose 11 points to 30.7 this month (see Chart 1). The current shipments index also rose 11 points, to 29.9 in September. More than 34 percent of the firms reported increases in shipments this month, while only 4 percent reported decreases. The index for new orders fell 7 points to a reading of 15.9. Nearly 31 percent of the firms reported increases in new orders this month, while 15 percent reported decreases.

On balance, the firms continued to report increases in employment, but the employment index declined from 32.6 in August to 26.3 this month. The majority of responding firms (62 percent) reported steady employment levels, and the share reporting increases (31 percent) exceeded the share reporting decreases (5 percent). The average workweek index climbed 5 points to 29.3.

Price Increases Remain Widespread

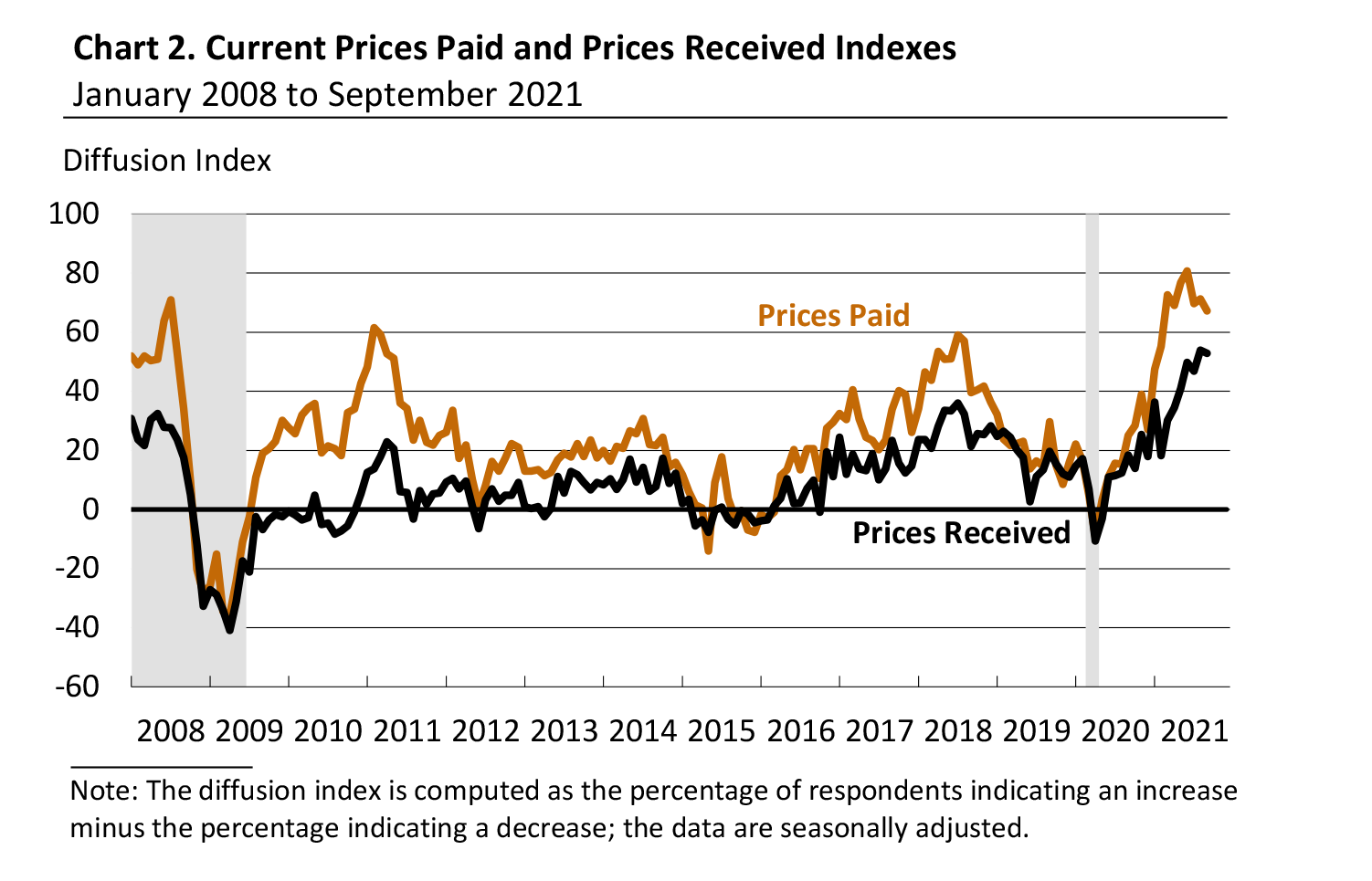

The indicators for prices paid and prices received remained elevated but posted small declines this month. The prices paid index declined 4 points to 67.3 (see Chart 2). The percentage of firms reporting increases in input prices (71 percent) far exceeded the percentage reporting decreases (4 percent); 23 percent of the firms reported no change. The current prices received index ticked down 1 point to 52.9. Nearly 55 percent of the firms reported increases in prices received for their own goods this month, 2 percent reported decreases, and 42 percent reported no change.

Firms Report Higher Production and Capacity Utilization

In this month’s special questions, the firms were asked to estimate their total production growth for the third quarter ending this month compared with the second quarter of 2021 (see Special Questions). The share of firms reporting expected increases in third-quarter production (70 percent) was greater than the share reporting decreases (18 percent), with a median response of an increase of 0 to 5 percent. The firms were also asked about their current capacity utilization rate as well as their utilization rate one year ago. The median current capacity utilization rate reported among the responding firms was 70 to 80 percent, higher than the median rate of 60 to 70 percent reported for one year ago. Most firms reported supply chain (87 percent) and labor (74 percent) issues as factors constraining current capacity utilization.

Firms Remain Optimistic About Growth

The diffusion index for future general activity decreased for the third consecutive month, falling 14 points to 20.0 (see Chart 1). The share of firms expecting increases in activity over the next six months (33 percent) exceeded the share expecting decreases (13 percent); a majority (41 percent) expect no change. The future new orders index declined 6 points, while the future shipments index inched up nearly 1 point. The firms continued to expect overall increases in employment over the next six months, although the future employment index declined 4 points to 38.6. Over 44 percent of the firms expect to increase employment in their manufacturing plants over the next six months; only 6 percent anticipate employment declines.

Summary

Responses to the September Manufacturing Business Outlook Survey suggest continued expansion in regional manufacturing conditions this month. The indicators for current activity and shipments rose from their August readings. The price indexes remain elevated and continue to suggest widespread increases in prices. The survey’s future indexes indicate that respondents continue to expect growth over the next six months, although the future general activity and new orders indexes continued to trend lower.

Special Questions (September 2021)

| 1. How will your firm’s total production for the third quarter of 2021 compare with that of the second quarter? | ||||

|---|---|---|---|---|

| An increase of: | % of firms | Subtotals | ||

| 20% or more | 7.5 | % of firms reporting an increase: 70.0 | ||

| 15-20% | 2.5 | |||

| 10-15% | 7.5 | |||

| 5-10% | 30.0 | |||

| 0-5% | 22.5 | |||

| No change | 12.5 | |||

| A decline of: | ||||

| 0-5% | 7.5 | % of firms reporting a decrease: 17.5 | ||

| 5-10% | 2.5 | |||

| 10% or more | 7.5 | |||

| 2. Which of the following best characterizes your plant's percentage capacity utilization currently (2021:Q3) compared with a year ago (2020:Q3)? | ||||

|---|---|---|---|---|

Capacity Utilization Rate |

2021:Q3 % of Reporters |

2020:Q3 % of Reporters |

||

| Less than 30% | 0.0 | 2.5 | ||

| 30-40% | 5.1 | 0.0 | ||

| 40-50% | 2.6 | 10.0 | ||

| 50-60% | 2.6 | 12.5 | ||

| 60-70% | 15.4 | 27.5 | ||

| 70-80% | 30.8 | 32.5 | ||

| 80-90% | 33.3 | 15.0 | ||

| 90-100% | 10.3 | 0.0 | ||

| Median Utilization Rate | 70-80 | 60-70 | ||

| 3. Have any of the factors below acted as constraints on capacity utilization this quarter?* | |

|---|---|

| % of Reporters | |

| Labor issues | 74.4 |

| Supply chain issues | 87.2 |

| COVID-19 mitigation measures (e.g., reduced operations, distancing) | 15.4 |

| Other factors | 7.7 |

| *Percentages will not add to 100 because more than one action could be selected. | |

Return to the main page for the Manufacturing Business Outlook Survey.